I have always been the kind of person who stands up for herself. It’s just something that I learned to do early on, and have gotten better at over the years.

What does it mean to “self-advocate?”

When you have a legitimate issue that is fixable, and you take it to the next level by contacting customer service or a manager, you are self-advocating.

By “taking it the next level”, I mean communicating politely. It doesn’t mean going all Liam Neeson on the issue.

Here are three examples of what I have been able to accomplish with a phone call:

1. I purchased a certain service while on vacation and felt mislead. The written description did not explain the service properly. If I had understood what they were saying (the way they meant it), I wouldn’t have bought it. So, I filled out the online survey and asked that the company call me. When they did, I explained what I understood the service to be and they clarified what it was supposed to be. After advocating for myself and politely saying that I didn’t think it was worded properly, they gave us a free dinner for two in a specialty restaurant the next time we sail on that cruise line.

2. I purchased a massage through a discount website but was unable to reach the massage therapist. I contacted the website and asked for assistance in getting a.) the appointment or b.) a refund. Everything was settled to my satisfaction, because I kept records of my attempts to contact the therapist (date, time of call and response).

3. I received a medical bill in the mail for services that were not covered by our insurance, months after the service date. I contacted the billing company to ask why they waited so long to bill me. They explained that they had let the billing person go and that they were behind in the billing. I explained my case, which was we have changed insurance companies since the time of the appointment and I didn’t know if I could go back and dispute the insurance claim since this was several months before. In addition, the H-S-A account we had with that insurance was now closed. We compromised and settled the bill for an amount which we both agreed was fair.

What you need to stand up for yourself

1. The will and desire to get what you paid for.

2. The ability to stay polite and calm. I can’t stress this enough. This isn’t about ruining someone’s day or getting something extra. It’s about establishing the facts – did you, or did you not, get what you paid for?

3. Documentation – What was purchased and when (a receipt is great), what is the issue, how often and when have you contacted the merchant.

If you are doing online chat with customer service, make sure you keep a copy of the chat transcript. I recently learned that if you are dealing with a merchant who records your calls, you can and should get a recording reference number as additional documentation. Even I can learn something new.

It doesn’t always work

You will never know if you don’t try. I think you need to try to get an amicable resolution that is fair to you and the other party. If not, you can always avoid that service in the future, or leave a negative (but fair) review.

Funded in part through a Cooperative Agreement with the U.S. Small Business Administration.

Funded in part through a Cooperative Agreement with the U.S. Small Business Administration.

Maclyne Josselin might catch the eye of any corporate comptroller looking to build a staff, keeping a ledger within arm’s reach in which she tracks income and expenses to the penny.

Maclyne Josselin might catch the eye of any corporate comptroller looking to build a staff, keeping a ledger within arm’s reach in which she tracks income and expenses to the penny.

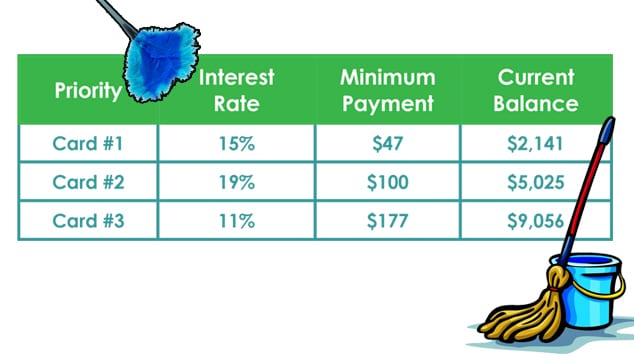

Do you know what’s really scary? Having company due in 5 minutes when the bathrooms aren’t clean. When that happens, do you lock the front door and pretend you’re not home? No! You walk into the bathroom and decide which part needs to be cleaned first (just in case you run out of time before the doorbell rings).

Do you know what’s really scary? Having company due in 5 minutes when the bathrooms aren’t clean. When that happens, do you lock the front door and pretend you’re not home? No! You walk into the bathroom and decide which part needs to be cleaned first (just in case you run out of time before the doorbell rings).