Norwalk Community College is offering College for Kids this summer. I will once again be teaching Teens and Money: Teens Personal Finance – July 13 to 17 – 5 mornings. This class is limited to 15, register today at 203-857-7080 so you don’t miss out.

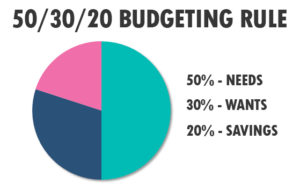

This is a general rule about spending – 50/30/20 rule. 50 percent of your take home income should go towards your needs (such as food, housing, childcare, minimum debt repayment etc.), 30% towards your wants (dining out, travel, clothing, subscriptions, memberships) and the remaining 20% to your savings / debt repayment (emergency funds, retirement, additional payments towards debt). Nerd Wallet can tell you the amount for each category

This is a general rule about spending – 50/30/20 rule. 50 percent of your take home income should go towards your needs (such as food, housing, childcare, minimum debt repayment etc.), 30% towards your wants (dining out, travel, clothing, subscriptions, memberships) and the remaining 20% to your savings / debt repayment (emergency funds, retirement, additional payments towards debt). Nerd Wallet can tell you the amount for each category  Like Capital One says, What’s in your wallet? Could you tell me everything that is in your wallet right now? If you were to lose your wallet today, how would you know what to cancel and replace. Clean out your wallet and carry only the minimum you require. You should never carry your social security card, your PIN numbers / passwords, blank check(s), passport unless you need to use them that day. Identity theft is on the rise. Protect yourself. #JillRussoFoster #FinancialLiteracyMonth

Like Capital One says, What’s in your wallet? Could you tell me everything that is in your wallet right now? If you were to lose your wallet today, how would you know what to cancel and replace. Clean out your wallet and carry only the minimum you require. You should never carry your social security card, your PIN numbers / passwords, blank check(s), passport unless you need to use them that day. Identity theft is on the rise. Protect yourself. #JillRussoFoster #FinancialLiteracyMonth Do you feel like you are spending too much? Have you considered an all-cash month? Or how about a no spending month? Here are two great books to read to give you some ideas Not Buying It: My Year Without Shopping by Judith Levine or The Complete Tightwad Gazette by Amy Dacyczyn. #JillRussoFoster #FinancialLiteracyMonth

Do you feel like you are spending too much? Have you considered an all-cash month? Or how about a no spending month? Here are two great books to read to give you some ideas Not Buying It: My Year Without Shopping by Judith Levine or The Complete Tightwad Gazette by Amy Dacyczyn. #JillRussoFoster #FinancialLiteracyMonth Have you cut the cord or do you want to with your TV provider or streaming service? When was the last time you used your local library? With your library card you can download the Hoopla app and stream movies at home for free. #JillRussoFoster #FinancialLiteracyMonth

Have you cut the cord or do you want to with your TV provider or streaming service? When was the last time you used your local library? With your library card you can download the Hoopla app and stream movies at home for free. #JillRussoFoster #FinancialLiteracyMonth Now that you are not paying fees on your bank account, are you earning interest on your money? There are some amazing accounts (both checking and savings) with great interest rates. Shop around for the best rate without fees. #JillRussoFoster #FinancialLiteracyMonth

Now that you are not paying fees on your bank account, are you earning interest on your money? There are some amazing accounts (both checking and savings) with great interest rates. Shop around for the best rate without fees. #JillRussoFoster #FinancialLiteracyMonth