We’ve all heard the word “refinance”, but what typically comes to mind is mortgages. Yes, you are correct. It also can apply to other areas of your finances such as car loans, student loans and credit cards.

As with any borrowing, you want to pay off the debt as quickly as possible. But sometime you cannot afford to purchase a car with cash, so you take a car loan. You may want to look into refinancing your car loan if you can get better terms – lower interest rate.

For student loans lower interest rate is probably not the answer. You may have several loans and several payments. It might be easier for you to keep track of and have only one payment per month, if you consolidate. Check out your options to determine if this is right for you.

Credit cards are a good example. You may be payoff debt and it may seem like it takes forever. It could if you have high interest rates. Refinancing a credit card balance to a lower or zero percent interest rate will help you pay back what you owe quicker and pay less in finance charges.

As with any financial transaction, do your research and compare all terms and conditions to see if this is the right move for you and your finances at this point in your life.

Maclyne Josselin might catch the eye of any corporate comptroller looking to build a staff, keeping a ledger within arm’s reach in which she tracks income and expenses to the penny.

Maclyne Josselin might catch the eye of any corporate comptroller looking to build a staff, keeping a ledger within arm’s reach in which she tracks income and expenses to the penny.

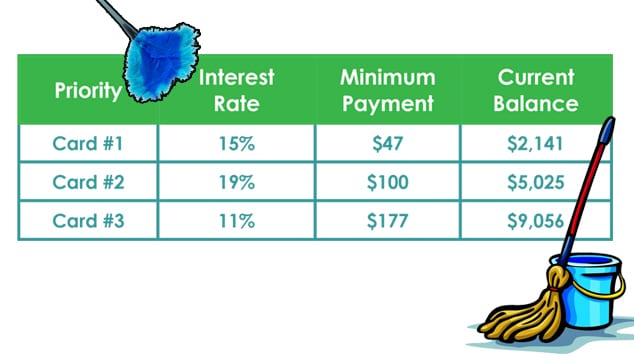

Do you know what’s really scary? Having company due in 5 minutes when the bathrooms aren’t clean. When that happens, do you lock the front door and pretend you’re not home? No! You walk into the bathroom and decide which part needs to be cleaned first (just in case you run out of time before the doorbell rings).

Do you know what’s really scary? Having company due in 5 minutes when the bathrooms aren’t clean. When that happens, do you lock the front door and pretend you’re not home? No! You walk into the bathroom and decide which part needs to be cleaned first (just in case you run out of time before the doorbell rings).