The first strawberries of the season! Organic, home-grown strawberries ready for the picking. All you pay for is the cost of the plants. These come back each year. Remember to use netting so the birds don’t get them first.

Tips for Successful Personal Finances

The first strawberries of the season! Organic, home-grown strawberries ready for the picking. All you pay for is the cost of the plants. These come back each year. Remember to use netting so the birds don’t get them first.

This is a great article about recent grads and tips for getting their first time job. Read more

Do you want your teen to start off their money and finances is a good way? Teach them to make choices that are right for them and come from a place of understanding. Give them the gift of Cash, Credit and Your Finances: The Teen Years. It’s simple to order at JillRussoFoster.com. If you want them book personalized to them, use this order form to order from us directly.

We love the beach. When we travel to a beach / pool destination, we bring along our own toys – noodles, rafts, snorkel gear and more. Not only does this save us money (much cheaper than buying at a hotel or destination), we always have what we want when we want it. This works because we have free checked luggage with our airline credit card. For more money saving tips visit www.JillRussoFoster.com and subscribe to our blog.

Do you want to save some money? We have replaced dryer sheets with wool dryer balls. As an added bonus these have no harmful chemicals. For more money saving tips visit www.JillRussoFoster.com and subscribe to our blog.

I always read these articles to make more changes to our finances

https://www.redbookmag.com/life/money-career/g4285/best-money-advice/

What do you think?

To start, we have been making better food choices over the past few years. As we get older, I want to still be active and healthy. This is a journey with small changes happening. We are striving for 50% of our plate to be vegetables. Our proteins are certified grass fed meats and fish with no antibiotics and non-GMO all while staying within our food budget. We shop what’s on sale and plan our meals to get the most from our dollars.

To start, we have been making better food choices over the past few years. As we get older, I want to still be active and healthy. This is a journey with small changes happening. We are striving for 50% of our plate to be vegetables. Our proteins are certified grass fed meats and fish with no antibiotics and non-GMO all while staying within our food budget. We shop what’s on sale and plan our meals to get the most from our dollars.

It’s that time of year to plan our garden and have fresh picked vegetables right in our backyard, at a minimal cost for organic seeds. Love this part of summer!

Here are some of our favorites to get more organic vegetables into our meals:

• Chicken Vegetable Soup making healthy bone broth with assorted vegetables. This is great to have on hand when we are short on time for dinner – just heat and eat.

• Lettuce wraps for lots of foods. Big leaf lettuce replaces the bread, wrap, taco and more. Inside can be anything from tuna to tacos – let your imagination run wild.

• Fries are one of my stress foods. But as I make these changes, there goes the fried foods. Now we bake or grill vegetable fries. Try it – avocado fries are one of favorites, but you can use many other veggies.

We are changing our food for the better. This wasn’t done overnight, just small changes (or baby steps) to gradually improve our choices. Our first step was to eliminate trans fats/partially hydrogenated oils, then came nitrates and then GMO’s. This exercise was eye-opening when I went through our pantry and even more surprising reading labels at the store.

As you can see, we are eating more at home and taking meals/snacks from home. Both are good things for our health and benefit our wallet too. More on the other areas of our lives that we have changed in the next issue.

Save

Save

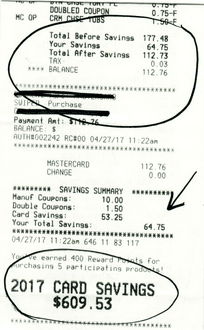

Don’t be in credit card debt. Make a plan to pay it off.

https://wallethub.com/edu/credit-card-debt-study/24400/