Do you ever seem to think, where is my money going? In 2025, we made lots of changes to our finances to reduce and/or eliminate expenses. According to a recent article from AARP, these hidden money leaks could be hazardous to your budget:

1, Automatically renewing your auto insurance: this is the next project for us. We are going to shop our home and auto insurance for better rates.

- Putting your internet on auto pilot: we switched providers last month and reduced our internet bills by two thirds. Yes, having to make an appointment for installation was a pain, but we have a guaranteed rate for three years that works for us.

- Paying for unused subscriptions

- Overspending on entertainment: we cut the cord on the triple play package and eliminated our home phone and cable TV. We are able to watch movies from our local Library with an app called Hoople for free,

- Overlooking bank fees: our bank accounts do not have any fees and neither should yours. We even earn interest on our checking account. We don’t pay a monthly fee and we don’t have to keep a certain amount to do that.

- Paying high credit card annual fees

- Leaving FSA funds behind: do you have an FSA (Flexible Spending Account)? If so, you have until the end of the year to use the funds to make purchases. If there is nothing you need to purchase, maybe stock up on over the counter medicines. You can also submit for reimbursement past expenses from the current year – copays, out of pocket costs, glasses / contact lens,

- Letting gift cards go to waste: you need to use or sell them before you lose them – the value doesn’t get lost, but you may misplace them.

For the full article click here.

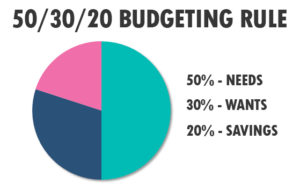

This is a general rule about spending – 50/30/20 rule. 50 percent of your take home income should go towards your needs (such as food, housing, childcare, minimum debt repayment etc.), 30% towards your wants (dining out, travel, clothing, subscriptions, memberships) and the remaining 20% to your savings / debt repayment (emergency funds, retirement, additional payments towards debt). Nerd Wallet can tell you the amount for each category

This is a general rule about spending – 50/30/20 rule. 50 percent of your take home income should go towards your needs (such as food, housing, childcare, minimum debt repayment etc.), 30% towards your wants (dining out, travel, clothing, subscriptions, memberships) and the remaining 20% to your savings / debt repayment (emergency funds, retirement, additional payments towards debt). Nerd Wallet can tell you the amount for each category  Do you have a surplus or deficit with your budget? We all know we can reduce or eliminate expenses. But sometimes this is not enough. Sometimes the answer will be that you need to increase your income or a combination of both. It’s something o think about. #JillRussoFoster #FinancialLiteracyMonth

Do you have a surplus or deficit with your budget? We all know we can reduce or eliminate expenses. But sometimes this is not enough. Sometimes the answer will be that you need to increase your income or a combination of both. It’s something o think about. #JillRussoFoster #FinancialLiteracyMonth If you want to track your spending, there are many ways to do this: pen and paper, receipts for all spending, use your debit / credit cards or an app to see where your money is going. If you would like a copy of my budget tracker formulated in Excel let me know and I will give you a copy. #JillRussoFoster #FinancialLiteracyMonth

If you want to track your spending, there are many ways to do this: pen and paper, receipts for all spending, use your debit / credit cards or an app to see where your money is going. If you would like a copy of my budget tracker formulated in Excel let me know and I will give you a copy. #JillRussoFoster #FinancialLiteracyMonth I would be remiss if I didn’t mention budgeting. When was the last time you tracked your spending? If you can’t remember when, it may be time to do this again. Learning where your money goes will help you to make changes so that you meet your goals. For example, “should I buy _______ or should I not spend this now and put it towards my goal of ____________.” #JillRussoFoster #FinancialLiteracyMonth

I would be remiss if I didn’t mention budgeting. When was the last time you tracked your spending? If you can’t remember when, it may be time to do this again. Learning where your money goes will help you to make changes so that you meet your goals. For example, “should I buy _______ or should I not spend this now and put it towards my goal of ____________.” #JillRussoFoster #FinancialLiteracyMonth Do you have an emergency fund? You never know what could happen in life. Experts say you should have 6 months to a year worth of income on hand for life’s what ifs. Yes, that can be overwhelming to go from minimal savings to this goal. Start by finding ways to save $5 a day to start. Automate your savings goals so that they happen. #JillRussoFoster #FinancialLiteracyMonth

Do you have an emergency fund? You never know what could happen in life. Experts say you should have 6 months to a year worth of income on hand for life’s what ifs. Yes, that can be overwhelming to go from minimal savings to this goal. Start by finding ways to save $5 a day to start. Automate your savings goals so that they happen. #JillRussoFoster #FinancialLiteracyMonth